Kriya Patel, CEO

Some might say not much has changed since the EU launched Open Banking two years ago. While estimates suggest one million UK consumers now use open banking products, that’s still under 2% of the population. In continental Europe, both the Berlin Group of 40 pan-European financial institutions and banking associations in Italy and Poland have started rolling out open banking roadmaps – as yet, though, few consumer products have been launched.

You could argue that low consumer adoption of open banking isn’t surprising given the challenges faced, including low awareness of the benefits, concerns about sharing personal data with service providers and the difficulties of managing ID verification between platforms.

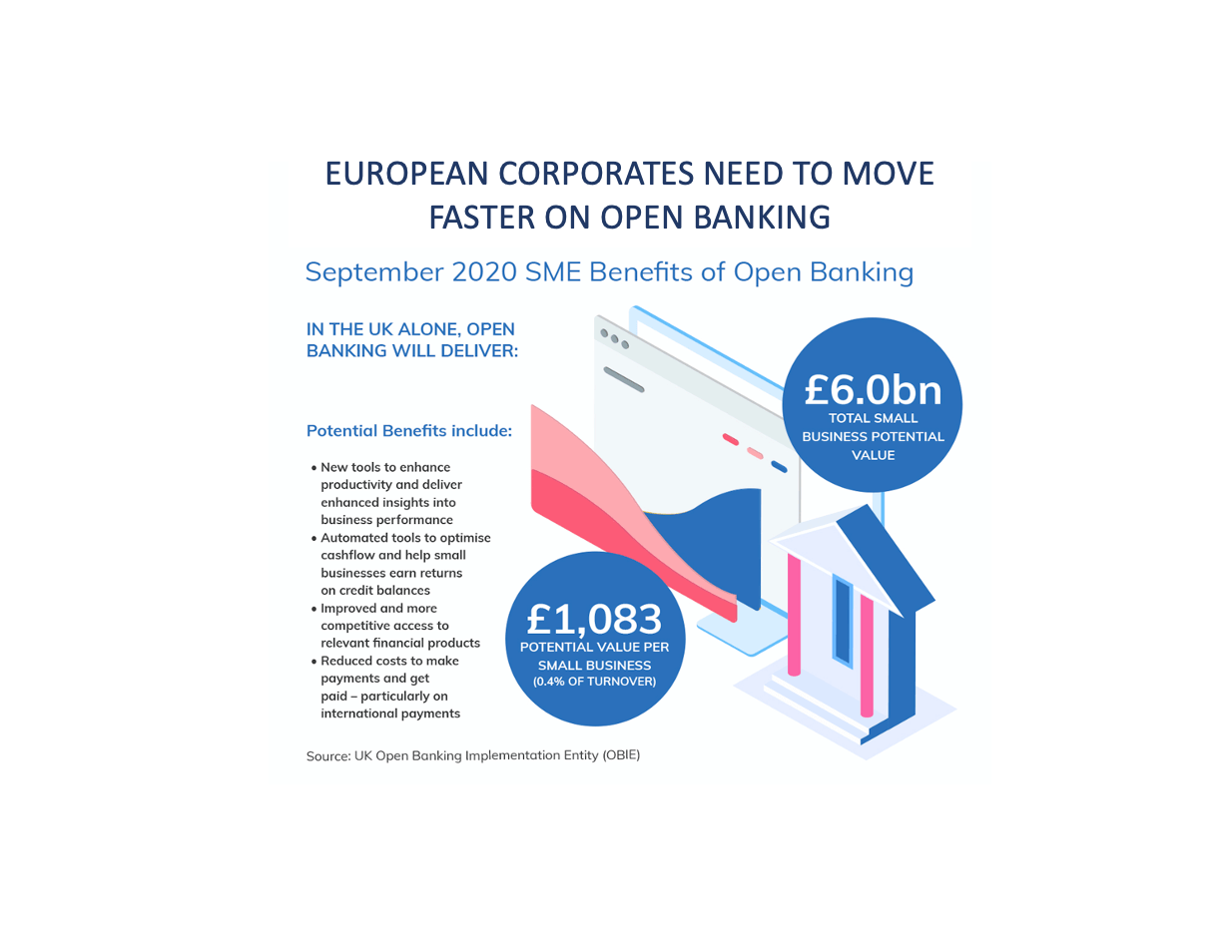

At TPL, we believe the first benefits of Open Banking will be realised in the business-to-business space. To start with, companies are more aware of open banking’s benefits and have greater trust around data confidentiality is. Secondly, banks are ready to serve their corporate customers – 95% of UK banks now have fully interoperable APIs and the capacity to share customer data. Although that figure drops to around 50% on the continent, the EU expects full compliance from banks by late 2021.

The challenge is that only 10 percent of Europe’s SMEs have fully digitized financial systems. Another 45% blend digital and manual – such as digital invoices mailed through the post – meaning that fully 45% of European companies use no digitisation at all. Open Banking is going to amplify the benefits of digitisation in B2B payments over the next two years, as well as creating new benefits – and companies must get ready, or risk being left behind.

“Open Banking is going to amplify the benefits of going digital over the next 2 years – and companies must get ready.”

By allowing corporates to onboard payments counterparties more quickly thanks to rich data exchanges with other banks, open banking is going to remove a lot of the friction companies currently experience. It will also reduce fraud rates in corporate banking, and make AML and fraud management easier. Corporate payments will become faster and cheaper internationally, too – whether through SEPA’s SCT-INST scheme or paired national Faster Payments Schemes.

Open Banking will also make it easier to identify counterparties via national company registers. At present, there’s no easy way for a company to acquire information on its counterparties – searches have to be done individually, and governments charge money for each search. However, as financial institutions connect to national registers via open APIs, these searches will become instantaneous. Looking further ahead, Open Banking is going to make invoice queries, product returns and tax disclosures easier and cheaper to execute as trusted counterparties are able to automatically interrogate each other’s invoicing and receivables records. However, all of these benefits will only be available to those with modern accounting and financial systems, including open APIs.

European companies must upgrade their accounting and financial systems as soon as possible, and engage with banks and payment service providers to make sure their systems are ready for open banking. Failure to do so could see companies missing out on the many opportunities open banking offers. If you’re not sure how to approach such an upgrade, a great place to start is to talk to an experienced service aggregator that can assess your current approach and advise on next steps.

Find out more about the Corporate Payment Solutions we offer at Transact Payments.

Regulated by the Gibraltar Financial Services Commission, Transact Payments Limited (TPL) has built a reputation as the go-to experts for payment and card solutions. For more, please visit: www.transactpaymentsltd.com

Share: